Fed Minutes Today May Signal September Rate Hike or Easing Ahead

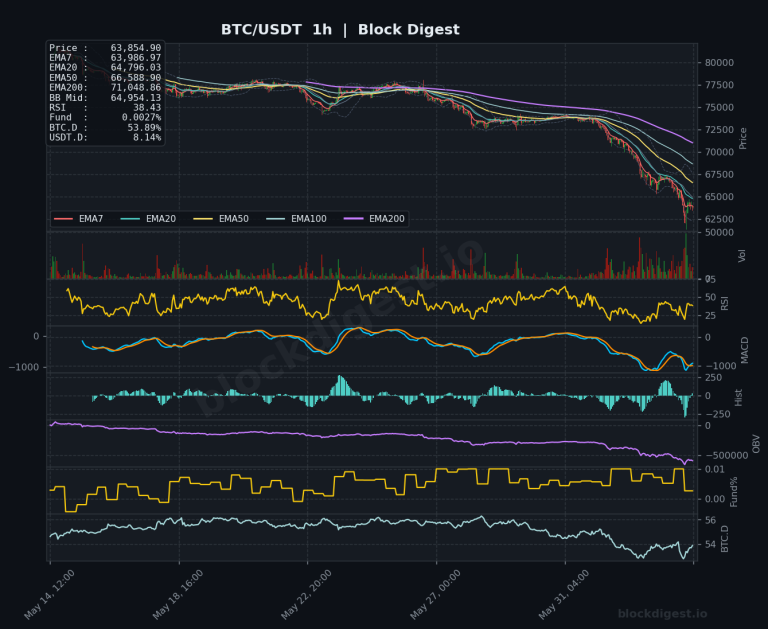

The Federal Reserve releases minutes from its June 16-17 policy meeting at 2:00 p.m. ET today, marking the most significant macro catalyst for cryptocurrency markets in the current 24-hour window. With Chair Kevin Warsh offering minimal forward guidance during the post-meeting press conference, the committee’s internal debate transcript becomes the primary vehicle for understanding whether a rate hike could arrive as soon as September. Bitcoin, which crashed below $57,000 last week, has stabilized near $63,000 as weaker employment data and moderating inflation signals have temporarily eased rate-hike concerns, but today’s minutes release is expected to produce sharp volatility across rate-sensitive assets.

Background: The Silent Fed and the Rate Hike Question

The Federal Reserve held its benchmark federal funds rate steady at 3.50 percent to 3.75 percent on June 17, maintaining the pause that has defined policy since late 2023. What distinguished this particular hold was the tone. The Committee removed earlier language suggesting that rate cuts could materialize soon and instead shifted its focus squarely toward bringing inflation back under control. That hawkish tilt surprised many investors who had priced in a more dovish stance heading into the summer.

The immediate puzzle for market participants was Chair Warsh’s deliberate reticence during the post-meeting press conference. Unlike his predecessors, Warsh offered little substantive commentary on the Committee’s thinking about 2026 rate movements. That silence created an information vacuum, one that the minutes—released today—are designed to fill. The internal committee transcript provides the only authoritative on-record statement from Federal Reserve officials about whether tightening could resume in the coming months.

The Committee’s Divided View on Rate Hikes

Nine of the 18 FOMC participants submitted dots in the June Summary of Economic Projections indicating support for at least one rate hike during 2026. That figure alone signals meaningful division within the Committee. However, the composition of those votes matters significantly. Knowing whether hawkish dots came from voting members, non-voting regional Fed presidents, or a mix of both will shape how traders interpret the Committee’s true center of gravity.

The median federal funds rate projection across all participants increased in June, implying that the Committee’s collective expectation tilted toward tightening rather than easing as the year progresses. By December 2026, CME FedWatch data shows traders are assigning roughly a 40 percent probability that rates could climb to 3.75 percent to 4.00 percent, up from the current 3.50 to 3.75 percent range. For the July 28-29 meeting, however, the market is pricing a hold at better than 75 percent probability, suggesting that any near-term hike would more likely occur in September at the earliest.

What Analysts Are Watching For

Market participants are focused on specific linguistic markers within the minutes that could signal hawkish or dovish intent. Repetition of the word “persistent” in reference to non-energy inflation carries particular weight, as does language such as “some firming may be appropriate.” These phrases function as coded forward guidance, telegraphing the Committee’s readiness to tighten policy if inflation data deteriorates.

A secondary focus is how the Committee discussed the macroeconomic effects of the ongoing Middle East conflict. That geopolitical risk could complicate the inflation picture if energy prices spike, forcing the Fed to balance hawkish impulses against potential growth headwinds.

The timing of today’s release also matters tactically. The June Consumer Price Index report is scheduled for July 14, six days after the minutes drop. If CPI data comes in hotter than expected, it would immediately reset rate-hike probabilities upward and contradict any dovish signals the minutes might contain. Conversely, a softer CPI reading would validate recent market optimism about moderating price growth.

Market Impact and the Bitcoin Context

Bitcoin’s price action over the past week reflects the growing bifurcation in Fed expectations. The July 3 employment report missed expectations significantly, with non-farm payrolls rising just 114,000—well below the 190,000 forecast. That soft labor data, combined with signs of moderating inflation, gave traders confidence that the Fed might maintain its current pause through year-end. Bitcoin rebounded from below $57,000 to trade near $63,000 in the days following the jobs report.

However, that recovery remains fragile and contingent on the Fed narrative staying dovish. A minutes release that emphasizes persistent inflation concerns or Committee members expressing readiness to hike could trigger a sharp repricing lower. FOMC minutes historically produce volatility in rate-sensitive assets including Bitcoin and Ethereum, as traders rapidly adjust their interest-rate terminal rate assumptions and discount future cash flows accordingly.

What This Means for the Market

Today’s release will determine whether the prevailing market narrative—that the Fed has completed its tightening cycle and may begin easing later in 2026—holds up under scrutiny, or whether a hawkish committee composition and inflation concerns force traders to price in another 25 basis point increase before year-end. Crypto markets should prepare for elevated volatility in the two hours immediately following the 2:00 p.m. ET release, with secondary shocks arriving on July 14 when June inflation data lands.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Cryptocurrency markets are highly volatile and unpredictable. All trading decisions should be made based on your own research and risk tolerance. Block Digest is not responsible for any financial losses incurred as a result of acting on this content.